ESG Digital Reporting

Quality data on a Company’s Environmental, Social and Governance is the next important milestone for XBRL.

Climate Change & Digital Reporting

COP26 in Glasgow drew the attention of the world on all facets of climate change — the science, the solutions, and the political will to act. Leaders, such as the French president, Emmanuel Macron demanded that CEO bonuses be based on their company’s environmental results. While investment firms lobbied for greater disclosure on sustainability.

This focus on how companies can be encouraged or mandated to support climate change initiatives fits with the UN Climate Action as climate friendly commerce is a major building block of the response to climate change, and conversely disincentivizing unsustainable, environmentally damaging, socially bad practices.

XBRL a Core Part of The Response

UBPartner, along with many others, believes that XBRL can play a very important role in the standardisation of ESG data and in particular “Sustainability measurement”, as how companies determine the costs and activities that effect their impact on environmental and social change, will determine the success and the effectiveness of ESG programmes at the national and international level.

But every XBRL reporting framework needs a Taxonomy. There are several major initiatives underway:

- In 2021, the EU adopted a proposal for a ‘Corporate Sustainability Reporting Directive (CSRD)’, which will require all large companies to disclose environmental and social information.

- These companies will be mandated to digitally ‘tag’ the reported information, so it is machine readable and would be audited (assurance) in a similar way to current Annual financial reports under ESEF.

- The draft standards are being developed by the European Financial Reporting Advisory Group (EFRAG). It has established a Sustainability Reporting Board and Technical Expert Group (TEG) to manage the process and to publish the first set of exposure drafts (EDs) sometime in the summer of 2023.

- ISSB is part of the IFRS Foundation and has published draft General Requirements and Climate-related Disclosure standards.

- The ISSB has merged the earlier pathfinding work of the Climate Disclosure Standards Board (CDSB) and of the Sustainability Accounting Standards Board (SASB).

- The ISSB has made initial proposals for an IFRS Sustainability Disclosure Taxonomy (ISDT), enabling structured electronic tagging of a company’s sustainability disclosures.

- The hope is to establish a comprehensive global baseline for sustainability disclosures. In order to reduce the existing and further fragmentation of sustainability disclosure requirements, reduce costs for data preparers and improve information usability for data users.

Who Will It Affect?

Filers

Around 50,000 of the largest companies will be affected by the CSRD requirement in Europe. While the US SEC is proposing to adopt the ISSB taxonomy for its sustainability reporting to the 13,000 listed US companies. In addition, there are projects being planned in many countries as far and wide as Korea, Chile, etc

Auditors

A key part of the ESG disclosures is assurance and therefore most frameworks will require the reports to be audited. Auditors will need to be familiar with the new requirements and acquire tools to help them review the reports. Work is already underway to develop the relevant auditing standards to support this.

Consumers

Many investment funds and financial indices claim to be ‘Sustainable’ but there is little or no factual evidence to back up these claims. XBRL-tagged data in the ESG reports will provide real data for investors to review these claims, compare companies, and adjust their portfolios.

XBRL for Developers

Adopting new technology, like XBRL, is always risky and there are many hidden costs. UBPartner offers a broad range of software and expertise to get your journey started with XBRL, including training and useful advice.

LET’S DISCUSS YOUR ESG REPORTING PROJECT

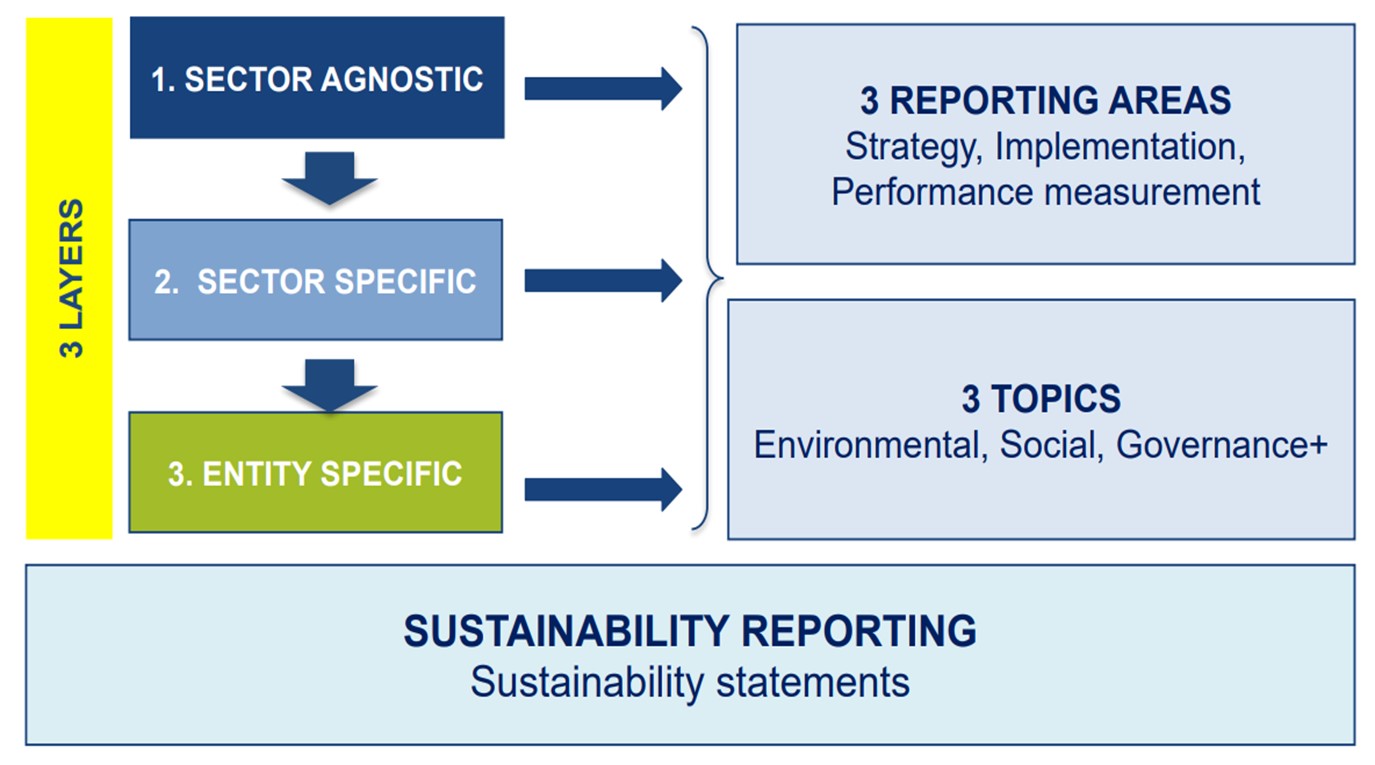

THE EUROPEAN TIMELINE

The Corporate Sustainability Reporting Directive (CSRD) initiative started in April 21 with a target adoption date of October 2024, suggesting that companies will be expected to provide initial Sustainability reports in 2025.

CSRD reporting will be based on a 3 layers approach, as shown in the diagram below.

A key goal of the project will be to look towards compatibility with the ISSB initiative.

Want more details on how our XBRL Tools can help?

XBRL Toolkit (XT) - Simple to use, Easy to deploy

XT Cloud Service - Let UBPartner manage it for you

XT Database - Analyse the data